Yes, in many cases, you can take a co-signer off your car loan, but it’s not a simple switch and requires meeting specific criteria and going through a formal process.

Having a co-signer on a car loan can be a lifeline, especially if your credit history isn’t stellar or you need a larger loan amount than you’d qualify for on your own. They essentially vouch for your ability to repay the loan, making lenders more comfortable. However, as your financial situation improves and your credit score climbs, you might find yourself wanting to sever that co-signing relationship. This guide will walk you through the ins and outs of removing a co-signer from your auto loan, covering the necessary steps, potential hurdles, and what to expect.

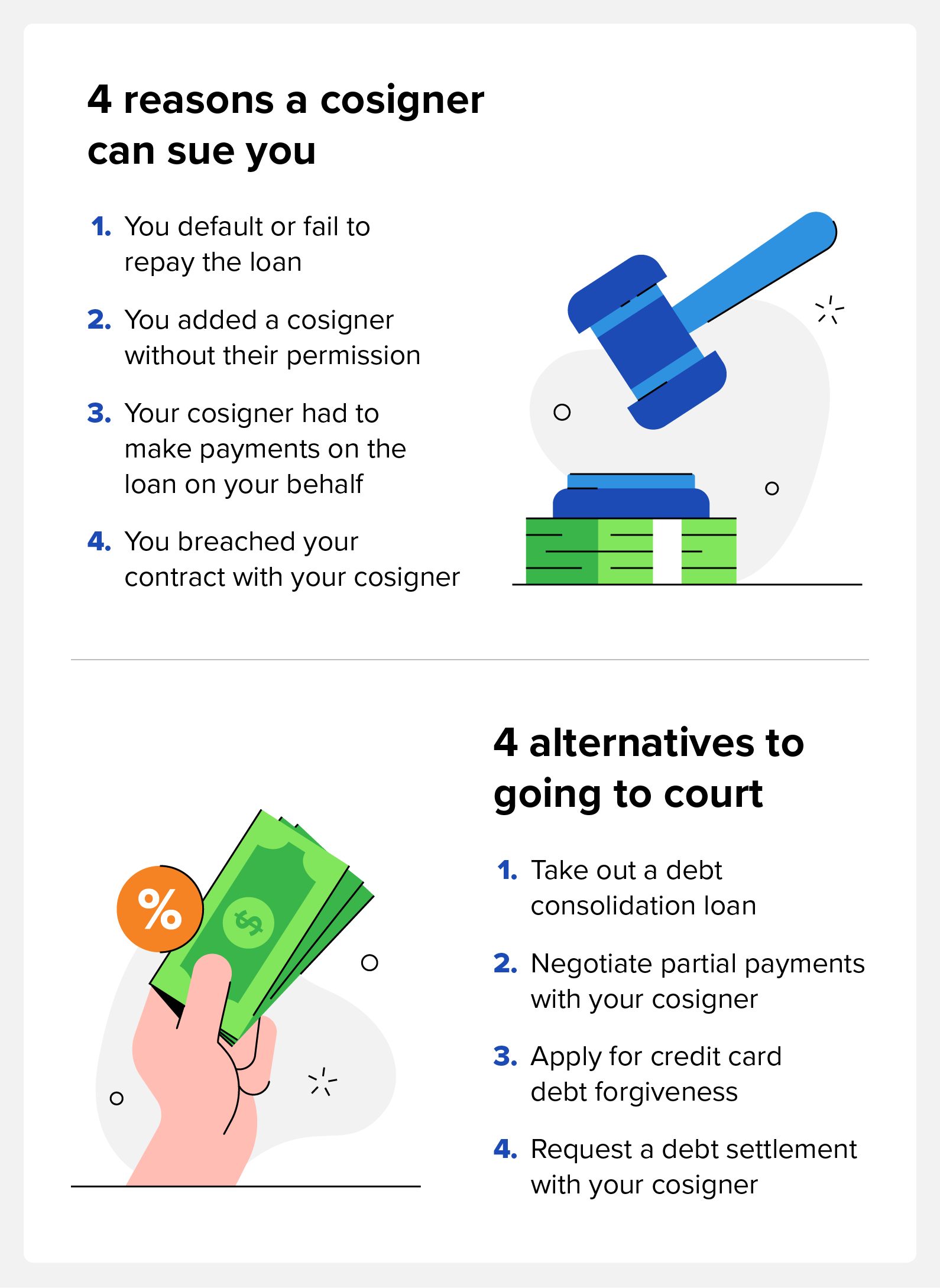

Image Source: www.credit.com

Why You Might Want to Remove a Co-Signer

Life changes, and so does your financial picture. Here are common reasons why someone might seek to remove a co-signer from their car loan:

- Improved Creditworthiness: Your credit score has increased significantly, making you a more attractive borrower on your own.

- Financial Independence: You want to solely manage your finances and debt without relying on another person’s credit.

- Relationship Changes: The co-signer is an ex-spouse, former partner, or even a friend, and the association is no longer desired or appropriate.

- Co-Signer’s Request: The co-signer may wish to have their name removed from the debt for their own financial planning, such as buying a house or improving their debt-to-income ratio.

- Clarity and Simplicity: Having one name on the loan simplifies financial records and responsibilities.

Deciphering the Co-Signer Agreement

A co-signer agreement is a legally binding contract. When someone co-signs your car loan, they are not just a helpful friend; they are equally responsible for the debt. This means:

- Shared Liability: If you miss payments, the lender can pursue the co-signer for the full amount owed, including late fees and interest.

- Impact on Credit: Missed payments or defaults will negatively affect both your credit score and the co-signer’s credit score.

- Credit Utilization: The loan debt counts towards the co-signer’s debt-to-income ratio, which can affect their ability to qualify for other loans or credit.

It’s crucial for both parties to fully grasp the implications of the co-signer agreement before signing.

Methods to Remove a Co-Signer from Your Car Loan

There are primary ways to achieve co-signer release from an auto loan:

1. Refinance the Car Loan

This is the most common and straightforward method. Refinancing involves applying for a new car loan, usually with better terms, and using the new loan to pay off the existing one.

How it Works:

- You apply for a new auto loan in your name only.

- The new lender pays off your old loan.

- You then make payments on the new loan.

- Your co-signer is removed from the obligation because the original loan is settled.

Eligibility for Co-Signer Removal Through Refinancing:

Lenders will assess your eligibility based on several factors:

- Credit Score: A higher credit score is essential. Lenders want to see a responsible payment history.

- Income and Employment Stability: You’ll need to demonstrate a stable income that can comfortably cover the new loan payments.

- Debt-to-Income Ratio (DTI): Lenders will calculate your DTI to ensure you aren’t overextended with other debts. A lower DTI makes you a more attractive borrower.

- Payment History: A consistent track record of on-time payments on your current car loan is critical.

Steps for Refinancing:

- Check Your Credit: Obtain copies of your credit reports from all three major bureaus (Equifax, Experian, TransUnion). Look for any errors and address them.

- Assess Your Financials: Gather proof of income (pay stubs, tax returns), bank statements, and a list of your current debts.

- Shop Around for Lenders: Compare offers from various banks, credit unions, and online lenders. Look at interest rates, loan terms, and fees.

- Apply for the Loan: Submit your application, providing all requested documentation.

- Close the Loan: Once approved, you’ll sign the new loan agreement, and the lender will disburse the funds to pay off the old loan.

- Update Title/Registration: If the loan is with a different bank, you might need to update the title and registration to reflect the new lienholder.

Pros of Refinancing:

- Removes the co-signer from the loan entirely.

- Potentially secures a lower interest rate or better loan terms.

- Improves your credit utilization and credit history by taking on new debt responsibly.

Cons of Refinancing:

- Requires good credit and stable income to qualify.

- May involve fees (origination fees, closing costs).

- If your credit hasn’t improved enough, you might not qualify or could end up with a higher rate.

2. Co-Signer Release Program

Some lenders offer a specific “co-signer release” program. This is a more direct route to removing a co-signer without a full refinance.

How it Works:

- You apply directly to your current lender to have the co-signer removed.

- The lender reviews your loan history and financial standing to determine if you meet their criteria for solo repayment.

Eligibility for Co-Signer Removal Through Release Programs:

Eligibility requirements vary significantly by lender but typically include:

- Minimum Payment Period: You’ve made a certain number of consecutive on-time payments (e.g., 12 or 24 months).

- Credit Score: Your credit score must meet the lender’s threshold for independent borrowers.

- Payment History: No late payments or defaults during the loan term.

- Loan-to-Value (LTV) Ratio: The amount you owe on the car should not exceed its current market value.

- Debt-to-Income Ratio (DTI): Your DTI must be within acceptable limits.

Steps for Co-Signer Release:

- Contact Your Lender: Inquire if they have a co-signer release program.

- Obtain Application: If they do, ask for the application form and list of requirements.

- Gather Documentation: Provide proof of income, credit information, and any other documents requested.

- Submit Application: Complete and submit the application to your lender.

- Approval: If approved, the lender will remove the co-signer from the loan contract.

Pros of Co-Signer Release Programs:

- Simpler process than refinancing with a new lender.

- Keeps the original loan terms in place if they are favorable.

- Can be easier to qualify for than a full refinance if your credit has only moderately improved.

Cons of Co-Signer Release Programs:

- Not all lenders offer this option.

- Requirements can be strict.

- The process can sometimes take a long time.

3. Auto Loan Buyout

This is less common for simply removing a co-signer and is more typically used when a co-signer wants to take ownership of the vehicle or when there’s a divorce settlement.

How it Works:

- One party (usually the primary borrower) pays off the entire remaining loan balance to free the vehicle from the lien.

- If the primary borrower wants to remove the co-signer and keep the car, they would need to secure new financing or use their own funds to pay off the loan. The co-signer would then sign over any ownership stake.

- If the co-signer wants to buy out the primary borrower and keep the car, they would need to get a new loan in their name (or use personal funds) to pay off the original loan and then transfer the title.

Eligibility for Auto Loan Buyout:

This method is primarily about having the funds to pay off the loan. The eligibility for new financing would follow standard lending criteria (credit score, income, DTI).

Steps for Auto Loan Buyout (to remove co-signer):

- Determine Payoff Amount: Get the exact payoff amount from your current lender.

- Secure Funds: Either use personal savings or secure a new loan to cover the payoff amount.

- Pay Off the Loan: Use the funds to pay the outstanding balance.

- Remove Lien: Once the loan is paid off, the lender will release the lien on the vehicle.

- Title Transfer (if necessary): If the co-signer was also on the title, you may need to complete a title transfer to remove their name.

Pros of Auto Loan Buyout:

- Completely removes the loan and any associated debt.

- Gives you full ownership of the vehicle.

Cons of Auto Loan Buyout:

- Requires significant funds to pay off the entire loan balance upfront.

- If you need new financing for the buyout, you’ll still need to qualify based on your credit.

The Co-Signer Credit Score Impact

A co-signer’s credit score significantly influences the loan approval process and the terms you receive. Conversely, their credit can also be impacted by the loan’s performance.

- Positive Impact: A co-signer with an excellent credit score can help you secure a lower interest rate, saving you money over the life of the loan.

- Negative Impact: If you miss payments, the late payments are reported to credit bureaus and will lower both your and your co-signer’s credit scores. This can also increase the co-signer’s debt-to-income ratio, making it harder for them to get approved for other credit.

Therefore, removing a co-signer is often beneficial for both parties, allowing the co-signer to improve their financial standing.

Transferring a Car Loan

While “transferring a car loan” might sound like a way to remove a co-signer, it’s not typically an option in the traditional sense. Lenders generally do not allow the outright transfer of an auto loan to another person’s name without a refinance or a new application. However, the concept of transferring responsibility is achieved through refinancing or a co-signer release.

What to Do If You Can’t Remove Your Co-Signer

If you’ve explored the options above and find that you’re not yet eligible to remove your co-signer, don’t despair. Focus on improving your financial standing:

- Continue Making On-Time Payments: This is the most crucial step. Consistent, timely payments build a positive payment history.

- Reduce Other Debts: Lowering your overall debt burden, especially credit card balances, will improve your debt-to-income ratio.

- Improve Your Credit Score: Pay bills on time, keep credit utilization low, and avoid opening new credit accounts unless necessary.

- Save for a Larger Down Payment (for Refinancing): A larger down payment on a new loan can improve your LTV ratio and make you a more attractive borrower.

- Communicate with Your Co-Signer: Keep them informed about your progress and your efforts to remove them from the loan.

Key Considerations Before Removing a Co-Signer

- Vehicle Ownership: Ensure the title reflects the correct ownership. Sometimes, a co-signer is also on the title. Removing them from the loan might necessitate a title transfer if they are also on it.

- Co-Signer’s Willingness: While you might want to remove them, ensure the co-signer is comfortable with the process and understands their responsibilities until the removal is complete.

- Lender Policies: Always confirm the specific policies and procedures with your lender, as they can vary.

Frequently Asked Questions (FAQ)

Q1: Can I remove my ex-spouse as a co-signer on my car loan?

Yes, you can often remove an ex-spouse as a co-signer, typically by refinancing the loan in your name only. The process requires you to qualify for the loan independently based on your credit and income.

Q2: Does removing a co-signer affect the car loan interest rate?

Yes, it can. If your credit score has improved since you initially took out the loan, refinancing to remove a co-signer might allow you to secure a lower interest rate. Conversely, if your credit has worsened, you might face a higher rate or be denied for the loan.

Q3: What happens if the co-signer wants to be removed, but I can’t qualify on my own?

If you cannot qualify to remove the co-signer, they will remain on the loan and responsible for its repayment. You would need to continue working on improving your credit and financial situation, or explore other options such as selling the car to pay off the loan.

Q4: Is there a fee to remove a co-signer?

There might be fees associated with refinancing the loan, such as origination fees or closing costs. If your lender has a specific co-signer release program, they may also charge an administrative fee. It’s important to inquire about any potential costs with your lender.

Q5: How long does it take to remove a co-signer?

The timeline can vary. Refinancing typically takes a few weeks from application to closing. A lender’s internal co-signer release program might take longer, potentially a month or more, depending on their processing times and documentation requirements.

Conclusion

Removing a co-signer from your car loan is a significant financial step towards greater independence. While it requires a commitment to building a strong financial profile and navigating a formal process, it is achievable for many. By understanding your options, preparing your finances, and diligently working with your lender, you can successfully achieve co-signer release and enjoy sole ownership of your auto loan obligations. Remember to always consult directly with your lender for the most accurate information regarding their specific policies and procedures.