Yes, you can often file for Chapter 7 bankruptcy and keep your car. The ability to keep your car in Chapter 7 bankruptcy depends on several factors, primarily the amount of equity you have in the vehicle and how you handle your car loan.

Filing for Chapter 7 bankruptcy can feel overwhelming, especially when you consider essential assets like your car. Many people rely on their vehicles for daily life – commuting to work, taking children to school, and handling everyday errands. The good news is that Chapter 7 bankruptcy doesn’t automatically mean losing your car. There are specific rules and strategies to help you protect your vehicle. This guide will delve into how you can navigate Chapter 7 and keep your car. We’ll explore exemptions, loan treatments, and the role of your local bankruptcy laws.

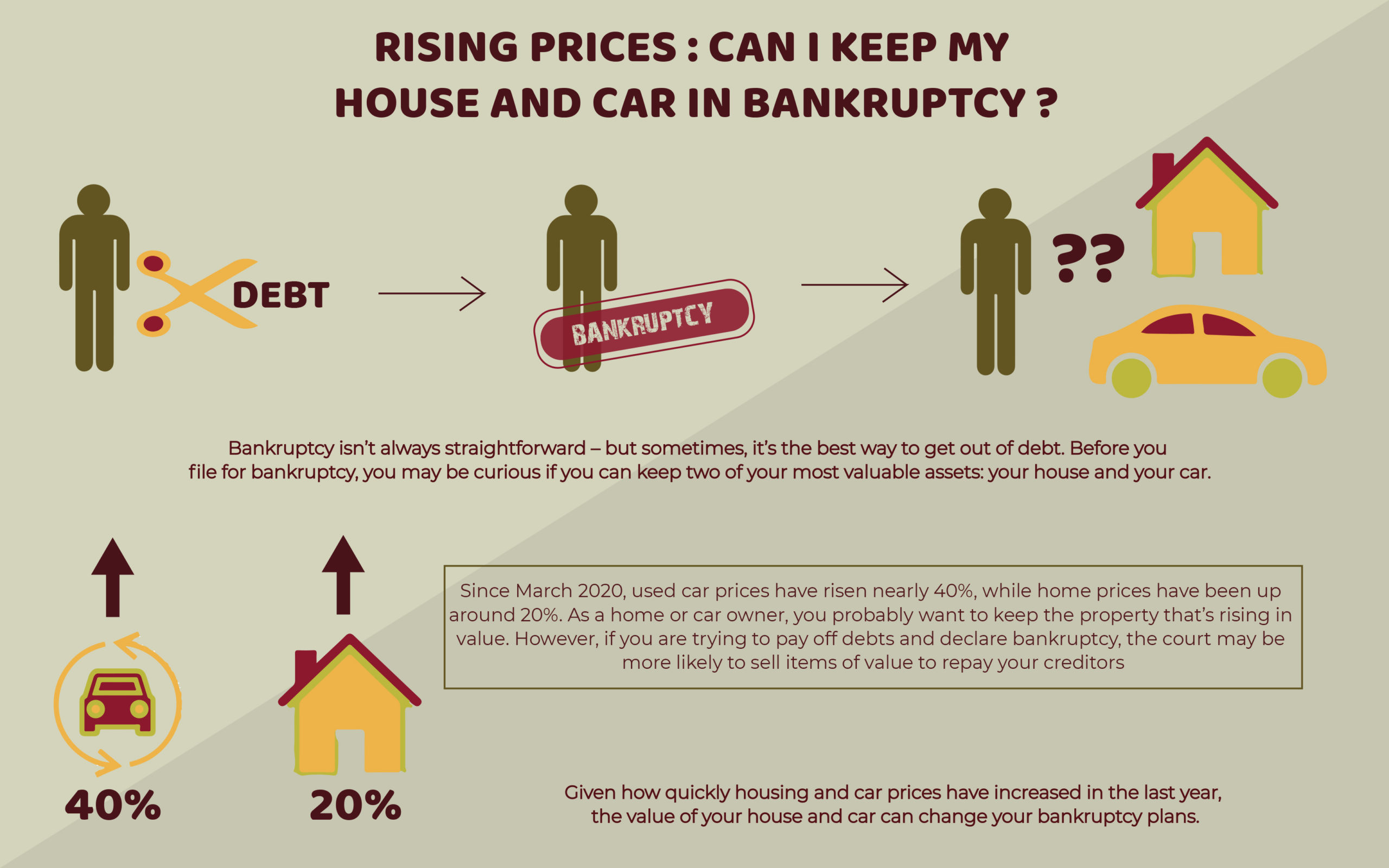

Image Source: www.therollinsfirm.com

Keeping Your Car in Chapter 7: The Core Concepts

The central idea behind keeping your car in Chapter 7 revolves around two main points: equity and car loan status. Bankruptcy laws allow individuals to protect a certain amount of value in their assets, and this protection extends to vehicles.

The Role of Equity in Chapter 7

Equity is the difference between the current market value of your car and the amount you owe on your car loan.

- Positive Equity: If you owe less than your car is worth, you have positive equity. For example, if your car is worth $10,000 and you owe $3,000, you have $7,000 in equity.

- Negative Equity: If you owe more than your car is worth, you have negative equity. For example, if your car is worth $5,000 and you owe $7,000, you have -$2,000 in equity.

The chapter 7 vehicle equity you possess is crucial because bankruptcy laws provide exemptions that protect a certain dollar amount of your assets. If your car’s equity falls within these exemption limits, you can typically keep it.

Your Car Loan and Chapter 7 Bankruptcy

How you handle your chapter 7 bankruptcy car loan is a key decision. You have a few options:

- Reaffirm the Loan: This means you agree to continue making payments on the car loan, and the debt will not be discharged in bankruptcy.

- Redeem the Car: You pay the lender the current market value of the car in a lump sum.

- Surrender the Car: You give the car back to the lender.

Each of these options has different implications for keeping your car during bankruptcy.

Chapter 7 Car Exemptions: What You Can Protect

Chapter 7 car exemption laws vary significantly from state to state, and there’s also a federal exemption scheme. You can generally choose to use either the federal exemptions or your state’s exemptions, whichever offers you better protection for your car.

Federal vs. State Exemptions

-

Federal Exemptions: The federal bankruptcy law provides a set of exemptions. The federal chapter 7 car exemption typically allows you to protect a certain amount of equity in your vehicle. As of 2023, the federal “wildcard” exemption, which can be used for any type of property, including vehicles, is quite generous. However, there is also a specific exemption for motor vehicles in some federal schemes, or the wildcard can be applied. It’s important to check the most current federal exemption amounts as they are adjusted periodically for inflation.

-

State Exemptions: Each state has its own set of exemptions. Some states offer very generous motor vehicle exemptions, while others may have lower limits. Some states allow you to “buy back” your vehicle by paying the non-exempt equity to the bankruptcy trustee. Other states have exemptions that are very high, essentially allowing anyone to keep their car regardless of its value, as long as they are making payments or the equity is low.

Important Note: If you live in a state that has opted out of the federal exemptions, you must use your state’s exemptions.

How Exemptions Work in Practice

Let’s say your state’s motor vehicle exemption is $5,000.

- Scenario 1: Low Equity: Your car is worth $6,000, and you owe $4,000 on the loan. Your equity is $2,000 ($6,000 – $4,000). Since your equity ($2,000) is less than the state exemption ($5,000), you can keep the car.

- Scenario 2: Moderate Equity: Your car is worth $12,000, and you owe $5,000 on the loan. Your equity is $7,000 ($12,000 – $5,000). Your equity ($7,000) exceeds the state exemption ($5,000) by $2,000. In this case, the $2,000 in non-exempt equity could be claimed by the bankruptcy trustee to pay off creditors. You would need to pay this $2,000 to the trustee to keep the car, or potentially negotiate a deal with the lender.

Understanding Your State’s Specific Exemptions

It is absolutely critical to know your state’s specific exemption limits for vehicles. You can find this information on government websites or by consulting with a bankruptcy attorney. The amounts can vary wildly.

Example of State Exemption Differences (Hypothetical):

| State | Motor Vehicle Exemption (Approximate) |

|---|---|

| State A | $5,000 |

| State B | $15,000 |

| State C | Unlimited (if used for work) |

As you can see, the state you reside in plays a massive role in whether you can keep your car.

Your Options for the Car Loan in Chapter 7

When you file for auto bankruptcy Chapter 7, you have distinct paths for handling your car loan. The choice you make will determine whether you can continue keeping your car during bankruptcy.

Option 1: Reaffirm Your Car Loan

Reaffirm car loan Chapter 7 is a common strategy for people who want to keep their car and can afford the payments.

What is Reaffirmation?

Reaffirmation is a legal agreement you make with your lender to continue paying your car loan even after your other dischargeable debts are eliminated in bankruptcy. You essentially “re-own” the debt.

How Does It Work?

- Agreement: You and the lender must agree to the reaffirmation.

- Court Approval: The bankruptcy court must approve the reaffirmation agreement. The court wants to ensure that reaffirming the debt doesn’t cause you undue hardship and that you can afford the payments. For individuals not represented by an attorney, a hearing is usually required. For those with attorneys, the attorney can certify that the agreement is in your best interest and doesn’t create undue hardship.

- Continuing Payments: You continue making your regular chapter 7 car payment as if bankruptcy never happened.

- No Discharge: The car loan debt is not discharged. If you stop paying later, the lender can repossess the car and potentially sue you for any deficiency balance.

Pros of Reaffirming:

- Keep Your Car: This is the primary benefit if you need the vehicle.

- Retain Ownership: You maintain clear ownership of the car.

- Potential Credit Building: Making consistent payments after reaffirmation can help rebuild your credit.

Cons of Reaffirming:

- Debt Remains: You are still legally obligated to pay the debt. If your financial situation changes, you could still face repossession.

- Risk of Deficiency: If the car is repossessed after reaffirmation, the lender can still pursue you for the difference between what you owe and what the car sold for at auction.

- Requires Court Approval: The court needs to agree it’s a reasonable decision.

When is Reaffirmation a Good Choice?

- You have significant positive equity in the car that is not covered by exemptions.

- You are current on your car payments and can comfortably afford them.

- You need the car for work or essential transportation.

Option 2: Redeem Your Car

Redeeming your car means you pay the lender the current market value of the car, not the total amount owed on the loan. This is only an option if you can pay the full amount in cash.

How Does Redemption Work?

- Lump Sum Payment: You must pay the lender the car’s fair market value in one lump sum.

- Court Approval: This typically requires a court order.

- Clear Title: Once paid, you receive a clear title to the car, free of the lender’s lien.

Pros of Redeeming:

- Pay Less Than You Owe: You can potentially save money if you have a high interest rate or owe significantly more than the car is worth.

- Keep Your Car: You retain ownership of the vehicle.

- Debt Elimination: The original loan is paid off and eliminated.

Cons of Redeeming:

- Requires Cash: This is the biggest hurdle. Most people filing Chapter 7 don’t have the cash to redeem their car.

- May Not Be Possible: If you owe more than the car is worth, redemption isn’t an option in the traditional sense unless the lender agrees to a modified loan which can be complex.

Option 3: Surrender Your Car

If you can’t afford the payments, have too much equity that you can’t protect with exemptions, or simply don’t want the car anymore, you can choose to return it to the lender.

What is Voluntary Surrender Car Chapter 7?

A voluntary surrender car Chapter 7 means you voluntarily give the car back to the lender before they have to repossess it.

How Does Surrender Work?

- Notification: You inform the lender that you are surrendering the vehicle.

- Return: You return the car to the lender’s designated location.

- Debt Discharge: The remaining balance on the loan is typically discharged in your bankruptcy.

Pros of Surrendering:

- Eliminates Car Payments: You no longer have to make monthly payments.

- Avoids Deficiency: If you surrender the car before it’s repossessed, and the lender sells it for less than you owe, you are generally not responsible for the difference (deficiency balance). However, this can be complex and it’s wise to get legal advice.

- Frees Up Funds: The money previously going to car payments can be used for other needs.

Cons of Surrendering:

- Loss of Vehicle: You no longer have the car for transportation.

- Impact on Credit: Surrendering a vehicle is a negative mark on your credit report, similar to repossession.

- Potential for Deficiency (If Repossessed): If the lender repossesses the car and sells it for less than you owe, they could still try to collect the difference from you if you didn’t surrender it voluntarily or if the bankruptcy rules allow it. It’s best to clarify this with your attorney.

Table: Comparing Loan Options

| Option | Keep Car? | Debt Status | Payment Requirement | Court Approval? | Pros | Cons |

|---|---|---|---|---|---|---|

| Reaffirm | Yes | Remains active | Yes (regular payments) | Yes | Keep car, ownership, potential credit build | Still owe debt, risk of deficiency, court needed |

| Redeem | Yes | Paid off (lump sum) | No (after lump sum) | Yes | Pay less, keep car, debt eliminated | Requires cash, only possible if car is worth it |

| Surrender | No | Discharged | No | No | Eliminate payments, avoid deficiency (if voluntary) | Lose car, negative credit impact, potential repossession issues |

Can I Protect My Car in Chapter 7 If I’m Behind on Payments?

This is a very common question for those considering auto bankruptcy Chapter 7. The answer is often yes, but it depends on your specific circumstances and state laws.

How Being Behind Affects Your Options

- If You Want to Reaffirm: If you are behind on payments, the lender is unlikely to agree to a reaffirmation agreement unless you catch up on the missed payments and pay any late fees. You’ll need to prove to the court that you can resume making the chapter 7 car payment on time.

- If You Want to Redeem: Being behind doesn’t necessarily prevent redemption, but you’ll still need the lump sum of cash to pay the car’s current value.

- If You Plan to Surrender: If you are significantly behind, surrendering the car might be your most straightforward option.

The “Ride-Through” Option (Sometimes Available)

In some jurisdictions, or under certain circumstances, you might be able to “ride through” the bankruptcy. This means you continue making your car payments without formally reaffirming the loan. The lender agrees not to repossess as long as you stay current.

- How it Works: You continue making your chapter 7 car payment. The loan is not discharged, nor is it reaffirmed. The lien remains on the car.

- Risks: This is a risky strategy because the lender is not legally obligated to continue servicing the loan if you don’t reaffirm. They could potentially repossess the car if you miss a payment, even if you are current before filing. This is why legal advice is crucial here.

arrears and Reaffirmation

To reaffirm a loan when you are behind, you generally need to pay all the past-due amounts, fees, and interest. The reaffirmation agreement will then reflect this catch-up payment. This can be a significant amount of money, making redemption or surrender more attractive options for some.

The Trustee’s Role in Your Car

The bankruptcy trustee is appointed by the court to oversee your case and ensure that your creditors are treated fairly.

What the Trustee Looks For

- Exempt Property: The trustee’s primary concern is to identify non-exempt assets that can be sold to pay creditors. If your car’s equity exceeds your state’s or the federal exemption limits, the trustee may be able to sell the car, give you the exempt amount, and use the rest to pay your creditors.

- Lien Status: The trustee will examine whether there are liens on your car (e.g., the car loan). If the car is fully secured by the loan, meaning you owe as much or more than it’s worth, the trustee generally won’t be interested in it because there’s no equity to seize.

How to Protect Your Car from the Trustee

- Claim Exemptions: Ensure you claim the appropriate chapter 7 car exemption for your state or the federal exemptions when you file your bankruptcy petition. This is a critical step in keeping your car in Chapter 7.

- Low or No Equity: If your car has very little or no equity, it’s usually not an asset a trustee would want to seize. The costs and hassle of selling the car often outweigh the potential recovery for creditors.

- Pay Non-Exempt Equity: If there is non-exempt equity, you might be able to negotiate with the trustee to pay that amount to the estate to keep the car.

Filing Chapter 7 and Keeping Your Car: A Step-by-Step Approach

Navigating the process of keeping your car in Chapter 7 requires careful planning and adherence to legal procedures.

Step 1: Assess Your Situation

- Car Value: Determine the current fair market value of your car. You can check sites like Kelley Blue Book (KBB) or Edmunds.

- Loan Balance: Find out exactly how much you owe on your car loan.

- Payment Status: Are you current on your payments, or are you behind?

- State Exemptions: Research your state’s specific chapter 7 car exemption limits.

Step 2: Consult a Bankruptcy Attorney

This is arguably the most important step. An experienced bankruptcy attorney will:

- Advise you on your state’s exemptions and the federal exemptions.

- Help you determine the best strategy for your car loan (reaffirm, redeem, or surrender).

- Guide you through the reaffirmation process if you choose that option.

- Ensure your paperwork correctly claims your exemptions.

- Represent you in court if necessary.

Step 3: File Your Bankruptcy Petition

When you file, you will list your car and your car loan information on the bankruptcy schedules. You will also declare which exemptions you are claiming.

Step 4: Lender’s Response and Your Decision

- Lender’s Intentions: After you file, your lender will be notified. They will typically inform you of their policy regarding loans for filers of auto bankruptcy Chapter 7.

- Making Your Choice: You will need to decide whether to reaffirm, redeem, or surrender the vehicle within a specified timeframe, usually 30 days after the meeting of creditors.

Step 5: Court Approval (If Reaffirming)

If you choose to reaffirm your car loan, you will need to file the reaffirmation agreement and attend a court hearing or have your attorney certify the agreement.

Step 6: Post-Bankruptcy

- If Reaffirmed: Continue making your chapter 7 car payment as agreed.

- If Redeemed: Ensure the lump sum payment is made.

- If Surrendered: Your obligation for that loan is discharged.

Frequently Asked Questions About Cars and Chapter 7

Q1: What happens if I stop making my car payments after filing Chapter 7?

Generally, you should continue making your car payments until you have decided how to handle the loan (reaffirm, redeem, or surrender) and the court has approved your chosen path. If you stop paying without reaffirming or making other arrangements, the lender can proceed with repossession.

Q2: Can I keep my car if I am upside down on the loan (owe more than it’s worth)?

Yes, you usually can keep your car if you are upside down on the loan, provided you are current on your payments and your state’s exemption for vehicles is sufficient to cover any small amount of equity, or if the trustee has no interest due to the lack of equity. The loan balance exceeding the car’s value means you have no equity that the trustee can seize. You would typically continue making payments without reaffirming (a “ride-through”) or surrender the car.

Q3: What if my car is financed by a buy-here-pay-here dealer?

Buy-here-pay-here (BHPH) dealers often have different contract terms. Some may require reaffirmation of the loan as a condition of keeping the car. It’s crucial to discuss your specific BHPH contract with your bankruptcy attorney, as these arrangements can sometimes be more complex than traditional car loans.

Q4: How long does it take to reaffirm a car loan in Chapter 7?

The reaffirmation process typically needs to be completed within 60 days of the Section 341 Meeting of Creditors, though extensions may be granted. This means the actual filing of the reaffirmation agreement and any court hearing usually happens within a few months of filing your bankruptcy petition.

Q5: What is the “automatic stay” and how does it affect my car?

The automatic stay is a powerful protection that goes into effect the moment you file for bankruptcy. It immediately stops most collection actions, including repossessions, foreclosures, wage garnishments, and lawsuits. This stay gives you breathing room to sort out your finances and decide how to handle your car loan without immediate threat of repossession. However, the stay is temporary for repossessions, and if you don’t make arrangements to keep the car, the lender can seek permission from the court to repossess it after the stay is lifted.

Q6: Do I need to have my car insured if I’m keeping it in Chapter 7?

Absolutely. You must maintain valid auto insurance, especially if you reaffirm your loan. Lenders will require proof of insurance. Failing to maintain insurance could be a violation of your loan agreement and could lead to repossession, even if you are making your payments.

Conclusion: A Path to Keeping Your Car

Filing for Chapter 7 bankruptcy does not mean forfeiting your car. By understanding chapter 7 car exemptions, the nuances of chapter 7 bankruptcy car loan options like reaffirm car loan chapter 7, and the importance of timely decisions, you can successfully navigate this process. Whether you choose to reaffirm, redeem, or even voluntary surrender car chapter 7, the goal is to make the best decision for your financial future while maintaining essential transportation. Always consult with a qualified bankruptcy attorney to ensure you are making informed choices tailored to your unique situation and jurisdiction. With careful planning and expert guidance, keeping your car during bankruptcy is a very achievable goal for many individuals.