Yes, a car can absolutely be totaled from a rear-end collision. The key factor is not just the type of accident, but the extent of the damage and the cost to repair it relative to the car’s pre-accident value.

Rear-end collisions are incredibly common on our roads. The impact can range from a minor fender-bender to a devastating crash. When a vehicle is struck from behind, a cascade of damage can occur, affecting not only the rear of the car but also potentially rippling forward through the chassis. This leads many car owners to wonder: can a rear-end collision really lead to their vehicle being declared a “total loss”? The answer is a resounding yes, and this article will delve into why and how this happens, covering everything from rear-end damage severity to total loss car valuation and the intricacies of estimating repair costs.

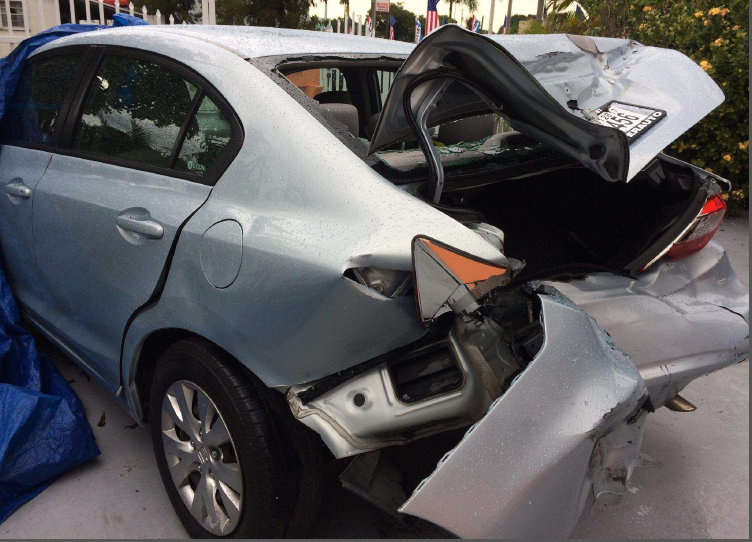

Image Source: www.jahlawfirm.com

Fathoming the Impact of Rear-End Accidents

A rear-end collision involves one vehicle striking the rear of another. While seemingly straightforward, the forces involved can be substantial and have far-reaching consequences for the vehicle’s integrity. The initial impact force is absorbed by the rear bumper, trunk, and rear frame. However, this force can then travel forward, affecting the undercarriage, suspension, powertrain, and even the cabin of the car.

Here’s a breakdown of common areas affected in a rear-end collision:

- Rear Structure: This includes the bumper cover, bumper reinforcement bar, trunk floor, and rear quarter panels. Damage here is almost a given.

- Frame and Unibody: The underlying structure of the car is critical. Even if the visible damage appears minor, the frame rails or unibody structure can be bent, twisted, or compromised. This is where the concept of structural integrity after crash becomes paramount.

- Suspension and Drivetrain: The impact can bend or break suspension components, such as control arms, axles, and shock absorbers. If the impact is severe enough, it can also damage the differential or transmission.

- Exhaust System: The exhaust pipes and muffler are often in the rear of the vehicle and can be crushed or torn away.

- Fuel Tank and Lines: While designed with safety in mind, a severe impact can potentially compromise the fuel tank or fuel lines, posing a fire risk.

- Electrical Components: Rear lights, sensors (like parking sensors or rear-view cameras), and wiring harnesses are all vulnerable.

- Interior: The rear seats, trunk liner, and even the rear of the front seats can be impacted by the force transferring forward.

Determining Vehicle Total Loss: The Insurance Perspective

Insurance companies employ a specific process to decide if a vehicle is a total loss. This isn’t just about the visible damage; it’s a financial calculation.

Total Loss Car Valuation: What’s Your Car Worth?

Before any repairs are considered, the insurance adjuster will determine the car’s Actual Cash Value (ACV). This is the market value of your vehicle immediately before the accident occurred. Factors influencing ACV include:

- Make and Model: The specific vehicle’s brand and model.

- Year: Older cars generally have lower ACVs.

- Mileage: Higher mileage typically means a lower ACV.

- Condition: The overall state of the car before the accident (e.g., wear and tear, previous damage, maintenance history).

- Features and Options: Higher trim levels or desirable options can increase value.

- Geographic Location: Market demand varies by region.

Insurance companies use various tools and databases, like Kelley Blue Book (KBB), NADA Guides, and local market data, to arrive at a fair ACV.

Estimating Repair Costs: The Crucial Calculation

Once the ACV is established, the next step is to obtain a detailed estimate of the repair costs from a qualified body shop. This estimate will include:

- Parts: The cost of all necessary replacement parts, from bumper covers to frame components.

- Labor: The cost of the technicians’ time to perform the repairs. This includes body work, painting, mechanical repairs, and reassembly.

- Associated Costs: This can include diagnostic fees, alignment, and any specialized procedures needed.

The “Total Loss” Threshold: When Repairs Don’t Make Sense

Insurance companies have a threshold for declaring a vehicle a total loss. This threshold varies by state and by insurance company, but it’s generally a percentage of the ACV. Common thresholds are:

- 70-75% Rule: If the estimated repair costs plus the estimated salvaged car value (the value of the wreck itself) exceed 70-75% of the ACV, the vehicle is typically declared a total loss.

- Total Loss Threshold Example:

- Let’s say your car’s ACV is $15,000.

- The estimated repair costs are $11,000.

- The estimated salvaged car value is $3,000.

- Total estimated cost = $11,000 (repairs) + $3,000 (salvage) = $14,000.

- If the threshold is 75%, then $14,000 is 93.3% of $15,000. Since this is over 75%, the car would likely be totaled.

It’s important to note that the insurance company considers the estimated repair costs. Sometimes, hidden damage is discovered once a car is disassembled for repair, which can increase the total cost.

Factors Influencing Rear-End Collision Severity and Total Loss Likelihood

The rear-end damage severity is the most direct determinant of whether a car will be totaled. Several factors contribute to this severity:

Speed of Impact

- High Speed: A higher speed impact generally results in more significant force and thus more extensive damage, increasing the likelihood of a total loss.

- Low Speed: While even low-speed impacts can be costly, they are less likely to cause frame damage severe enough to total a car unless the vehicle is older or already has underlying structural issues.

Vehicle Type and Construction

- Body-on-Frame vs. Unibody: Trucks and older SUVs built on a body-on-frame chassis might withstand impacts differently than unibody cars. However, severe impacts can still compromise frame integrity. Modern unibody vehicles are designed to absorb and dissipate energy through crumple zones, but if these zones are overloaded, the entire structure can be deemed irreparable.

- Vehicle Size and Weight: A smaller car being rear-ended by a larger vehicle will often sustain more severe damage.

Pre-Existing Damage or Age

- Older Vehicles: Cars that are older, have higher mileage, or have a history of previous repairs might have compromised structural integrity after crash. Rust or wear can weaken components, making them more susceptible to catastrophic damage.

- Previous Repairs: If the rear of the car has been repaired before, especially if it wasn’t done to factory specifications, it might be more prone to significant damage in a subsequent collision.

Specific Damage Components

- Frame Damage: This is a major red flag. If the main frame rails or unibody structure are bent, kinked, or compromised, the repair process becomes extremely complex and expensive. Many insurers will total a vehicle if significant frame repair is required. This is a critical aspect of collision damage assessment.

- Suspension Damage: Extensive suspension damage, especially if it affects multiple components or requires realignment of critical suspension points, can quickly drive up repair costs.

- Powertrain Damage: If the impact forces the engine or transmission rearward, causing damage, this can also contribute to a total loss declaration.

The Write-Off Process: What Happens When Your Car is Totaled?

When an insurance company declares your vehicle an accident vehicle write-off, they are essentially stating that the cost to repair it exceeds its economic value. Here’s what typically happens:

- Notification: The insurance adjuster will inform you that your car is a total loss. They will provide you with their valuation report for the ACV.

- Settlement Offer: The insurance company will offer you the ACV of your vehicle, minus your deductible.

- Taking Ownership: If you accept the offer, the insurance company will typically take possession of the damaged vehicle. They will then sell it at a salvage auction to recoup some of their costs.

- Keeping the Car (Salvage Title): In some cases, you may have the option to keep the totaled vehicle. If you choose this route, the insurance company will deduct the salvaged car value from your settlement offer. Your car will then be issued a salvage title, meaning it cannot be legally driven on the road until it is repaired and passes a stringent inspection (which varies by state). Driving a car with a salvage title without proper titling and inspection is illegal.

Insurance Payout for Totaled Cars: Your Compensation

The insurance payout for totaled cars is based on the ACV. It’s crucial to review the valuation report carefully. If you believe the ACV is too low, you have the right to negotiate.

- Gather Evidence: Compile your own research on your car’s market value, including comparable vehicles for sale in your area and any records of recent maintenance or upgrades that increase its value.

- Negotiate: Present your evidence to the adjuster. Be polite but firm. Many initial offers are negotiable.

- Independent Appraisal: If negotiations fail, you may consider obtaining an independent appraisal of your vehicle’s ACV.

Repairing vs. Totaling: A Cost-Benefit Analysis

The decision to repair or total a car boils down to economics.

When Repair is the Better Option

- Minor to Moderate Damage: If the rear-end damage severity is limited to cosmetic issues like a bumper cover, tail lights, and perhaps some minor trunk panel work, and the underlying structure is sound, repairs are usually feasible and cost-effective.

- Valuable Vehicle: For a high-value or classic car, even significant damage might be repairable if the repair cost is still less than a substantial percentage of its high ACV.

- Sentimental Value: While insurance payouts are based on market value, some owners might choose to pay the difference between the ACV and repair costs for a vehicle with deep sentimental value, provided it’s structurally sound.

When Totaling is Likely

- Significant Frame or Unibody Damage: This is the most common reason for a car to be totaled after a rear-end collision. Repairing modern unibody structures to their original structural integrity after crash is incredibly complex and expensive, often involving specialized equipment and extensive labor.

- Multiple Systems Damaged: If the impact affects the frame, suspension, drivetrain, and other critical systems, the accumulation of repair costs can quickly exceed the vehicle’s value.

- Older Vehicles with Low ACV: Even moderate damage can result in a total loss for older vehicles with low market values.

The Role of the Body Shop and the Insurance Adjuster

The initial collision damage assessment is usually performed by an insurance adjuster. However, they often rely on estimates from certified repair shops.

- Body Shop Expertise: Experienced body shops can identify all damage, including hidden issues, and provide accurate estimating repair costs. It’s wise to get estimates from a few reputable shops.

- Supplementals: If a body shop discovers additional damage during the repair process that wasn’t on the initial estimate, they will submit a “supplemental claim” to the insurance company for approval. This is another point where repairs might push the cost into total loss territory.

Can You Fight a Total Loss Declaration?

Yes, you can challenge a total loss declaration, especially if you believe the ACV is undervalued or the repair estimate is inflated.

- Challenge the ACV: As mentioned, gather evidence of your car’s market value.

- Question the Repair Estimate: If you have your own estimate from a trusted body shop that is significantly lower than the insurer’s estimate, you can present it for consideration. Ensure your estimate is detailed and addresses all the damage.

- Independent Inspection: In some cases, you might opt for an independent automotive appraiser to assess the damage and provide a repair estimate.

FAQs About Rear-End Collisions and Total Losses

Here are some common questions people have:

Q1: If my car has frame damage from a rear-end collision, is it always totaled?

A1: Not always, but it’s a very strong indicator. If the frame damage is minor and can be repaired to factory specifications without compromising structural integrity after crash, it might be repaired. However, significant frame damage is very expensive to fix correctly and often leads to an accident vehicle write-off.

Q2: How long does the total loss process usually take?

A2: The process can vary, but typically it takes anywhere from a few days to a couple of weeks once the damage has been assessed and the valuation is agreed upon. Delays can occur if there are disputes over the ACV or if additional damage is found.

Q3: What is a “salvage title” and should I keep a totaled car?

A3: A salvage title means the vehicle has been declared a total loss by an insurer. Keeping it means the insurance payout will be reduced by its salvaged car value. You can only legally repair and drive a car with a salvage title after it undergoes a rigorous inspection and is re-titled as “rebuilt.” Many people avoid this due to the complexity and potential for underlying issues.

Q4: Can a car be totaled from a rear-end collision even if it looks okay from the outside?

A4: Yes, absolutely. The most critical damage in rear-end collisions is often to the underlying structure, like the frame or unibody. This damage might not be visible until the car is inspected more thoroughly or partially disassembled, impacting its structural integrity after crash.

Q5: What is “diminished value” and do I get compensated for it if my car is repaired?

A5: Diminished value is the reduction in your car’s market value after it has been repaired following an accident, even if the repairs are perfect. This is because a vehicle with an accident history is generally worth less than one that has never been in a collision. While you receive an insurance payout for totaled cars based on its pre-accident value, compensation for diminished value is typically only pursued if the other party was at fault and you are dealing with their insurance. It’s often a separate negotiation and not always recoverable from your own insurer.

Q6: What happens to my loan if my car is totaled?

A6: If you have a loan on your vehicle, the insurance payout will first go towards paying off the outstanding loan balance. If the payout exceeds the loan balance, you will receive the remaining amount. If the payout is less than the loan balance (i.e., you owe more than the car was worth), you will still owe the remaining amount to the lender, unless you have GAP insurance, which covers this difference.

Q7: How does the impact of rear-end accidents affect the car’s safety features?

A7: Modern cars have sophisticated safety systems, including airbags, crumple zones, and anti-lock braking systems. A severe rear-end collision can damage these systems, including sensors for airbags or even the airbags themselves, further contributing to the estimating repair costs and the decision to total the vehicle. The structural integrity after crash is vital for all these systems to function correctly.

In conclusion, a rear-end collision can indeed lead to a car being totaled. It’s a decision driven by the economic reality of repair versus replacement, heavily influenced by the rear-end damage severity, the total loss car valuation, and the accuracy of estimating repair costs. Always communicate with your insurance adjuster, get second opinions on estimates if needed, and ensure you understand your vehicle’s true market value before agreeing to a settlement.